Pratham EPC Projects Limited IPO Subscription and Allotments

Pratham EPC Tasks Initial public offering is a book constructed issue of Rs 36.00 crores. The issue is completely a new issue of 48 lakh shares.

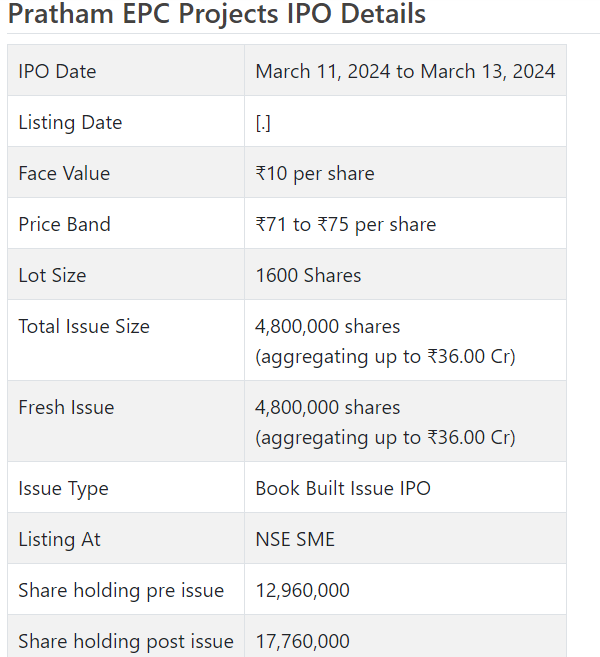

Pratham EPC Tasks Initial public offering opens for membership on Walk 11, 2024 and closes on Walk 13, 2024. The assignment for the Pratham EPC Tasks Initial public offering is supposed to be settled on Thursday, Walk 14, 2024. Pratham EPC Ventures Initial public offering will list on NSE SME with conditional posting date fixed as Monday, Walk 18, 2024.

Pratham EPC Tasks Initial public offering cost band is set at ₹71 to ₹75 per share. The base parcel size for an application is 1600 Offers. The base measure of venture expected by retail financial backers is ₹120,000. The base parcel size venture for HNI is 2 parts (3,200 offers) adding up to ₹240,000.

• PEPL is an arising player in gas pipeline infra with significant spotlight on crosscountry projects.

• It has eminent client list that incorporates Adani, GAIL, HPCL, BPCL and so forth.

• The organization checked development from FY23 ahead with its engaged crosscountry projects.

• In view of FY24 annualized profit, the issue shows up sensibly estimated.

• Financial backers might stop assets for the medium to long haul rewards.

ABOUT Organization:

Pratham EPC Ventures Ltd. (PEPL) is a coordinated designing, acquisition, development and dispatching organization being ready to go of start to finish specialist co-ops to Oil and Gas dispersion organizations in India. The organization has been executing different gas pipeline project dealing with all pipeline exercises like, mainline welding, tie-in, covering, hydro testing, pipeline appointing and so on. PEPL represents considerable authority in oil and gas pipelines for crosscountry dissemination and city gas conveyance. It likewise embraces seaward tasks for water appropriation explicitly project offering and venture the board.

PEPL is an Oil and Gas pipeline foundation specialist organization in India, zeroed in on laying pipeline networks alongside development of related offices; and giving Activities and Support administrations to the City Gas Circulation (“CGD”) Organizations in India. It is a coordinated EPC organization offering a broadened scope of pipeline and united administrations for oil and gas industry. It offers types of assistance for crosscountry pipeline projects for various applications viz. Oil, gas and water and so on and furthermore attempt Pipeline laying work on Turnkey premise including designing, obtainment, pipeline development for city gas dissemination, level bearing penetrating, stations including common, electromechanical and instrumentation for clients.

The organization is ISO 10002:2018 confirmed for consumer loyalty and grievance the board framework by Global Principles Enrollments, ISO 14001:2015 guaranteed for climate the executives framework by Worldwide Guidelines Enlistments, ISO 18001:2007 ensured for Word related Wellbeing and Security the executives framework by Worldwide Norms Enrollments and ISO 9001:2015 affirmed for quality administration framework by ROHS Affirmation Private Restricted. Its client list incorporates prestigious corporates like ONGC, BPCL, HPCL, Gujarat Gas, GAIL, Adani and so on and is as of now having significant spotlight on crosscountry gas pipe line projects.

Throughout the long term, it has effectively executed in excess of 12 undertakings with its major finished projects measuring to roughly Rs. 131.84 cr. Its execution capacities have developed fundamentally with time, both regarding the size of ventures that it offers for and execute, and the quantity of undertakings that it executes all the while. As of February 23, 2024, the organization had 8 significant on-going ventures out of which 7 undertakings worth roughly Rs. 296.66 cr. has been affirmed in light of Letter of Designation/Buy Request for which Rs. 240.16 cr. worth venture execution is forthcoming and 1 undertaking has been finished with Buy Request, which is worth around Rs. 406.67 cr., in light of the board gauges, serious areas of strength for proposing book. As of September 30, 2023, it had 770 workers on its finance.

ISSUE Subtleties/CAPITAL HISTORY:

The organization is emerging with its lady book building course Initial public offering of 4800000 value portions of Rs. 10 each to assemble Rs. 36.00 cr. (at the upper cap). It has reported a value band of Rs.71-Rs.75 per share. The issue opens for membership on Walk 11, 2024, and will close on Walk 13, 2024. The base application to be made is for 1600 offers and in products consequently, from that point. Post distribution, offers will be recorded on NSE SME Arise. The issue is 27.03% of the post-Initial public offering settled up capital of the organization. From the net returns of the Initial public offering, it will use Rs. 8.84 cr. for acquisition of apparatus, Rs. 15.15 cr. for working capital and the rest for general corporate purposes.

The issue is exclusively lead overseen by Direct path Capital Counselors Pvt. Ltd., and Connection Intime India Pvt. Ltd. is the enlistment center of the issue. Direct route Gathering’s Spread X Protections Pvt. Ltd. is the market creator for the organization.

The organization has given whole value capital at standard up to this point and has likewise given extra offers in the proportion of 15 for 1 in July 2023. The typical expense of securing of offers by the advertisers is Rs. 0.62 per share.

Post-Initial public offering, organization’s ongoing settled up value capital of Rs. 12.96 cr. will stand upgraded to Rs. 17.76 cr. In view of the upper Initial public offering cost band, the organization is searching for a market cap of Rs. 133.20 cr.

Monetary Execution:

On the monetary execution front, for the last three fiscals, the organization has posted an all out pay/net benefit of Rs. 30.85 cr. /Rs. 1.13 cr., (FY21), Rs. 50.63 cr. /Rs. 4.41 cr. (FY22), and Rs. 51.67 cr. /Rs. 7.64 cr. (FY23). For H1 of FY24 finished on September 30, 2023, it procured a net benefit of Rs. 5.23 cr. on an all out pay of Rs. 35.81 cr.

On a solidified premise, for the last two fiscals, it posted an all out pay/net benefit of Rs. 50.63 cr. /Rs. 4.42 cr. (FY22), and Rs. 51.69 cr. /Rs. 7.66 cr. (FY23). For H1 of FY24 finished on September 30, 2023, it procured a net benefit of Rs. 5.24 cr. on an all out pay of Rs. 36.30 cr. However it checked static top lines for FY22 and FY23, it stamped quantum bounce in its primary concern, that causes a stir. The flood went on for H1 of FY24 too. As indicated by the administration, this is credited to their significant spotlight on crosscountry high edge projects.

For the last three fiscals, it has revealed a normal EPS of Rs. 4.23, and a typical RONW of 38.66%. The issue is estimated at a P/BV of 4.19 in light of its NAV of Rs. 17.91 as of September 30, 2023, and at a P/BV of 2.25 in light of its post-Initial public offering NAV of Rs. 33.34 per share (at the upper cap).

On the off chance that we quality annualized FY24 income to its post-Initial public offering completely weakened paid-p capital, then the asking cost is at a P/E of 12.71.

For the announced periods, the organization has posted PAT edges of 3.69% (FY21), 8.74% (FY22), 15.22% (FY23), 15.26% (H1-FY24), and RoCE edges of 27.40%, 61.54%, 48.40%, 24.81% separately for the alluded periods.

Profit Strategy:

The organization has not proclaimed any profits for the announced times of the deal record. It will embrace a judicious profit strategy in light of its monetary presentation and future possibilities.

Correlation WITH Recorded Friends:

According to the deal report, the organization has shown Likhitha Infra as their recorded companions. It is exchanging at a P/E of 16.4 (as of Walk 05, 2024). Nonetheless, they are not practically identical on an apple-to-apple premise.

Shipper BANKER’S History:

This is the 32nd command from Direct route Capital in the last two fiscals, out of the last 10 postings, all opened at expenses going from 6.58% to 200.00% on the date of posting. Notwithstanding, the proposition archive is feeling the loss of its year-wise count data.

End/Speculation Technique

The organization is arising player in gas pipeline foundation related benefits and making progress with its crosscountry centered projects. It checked flood in benefits from FY23 onwards with its changed technique. It has great client list. In light of FY24 profit, the issue shows up sensibly valued. Financial backers might stop assets for the medium to long haul rewards.